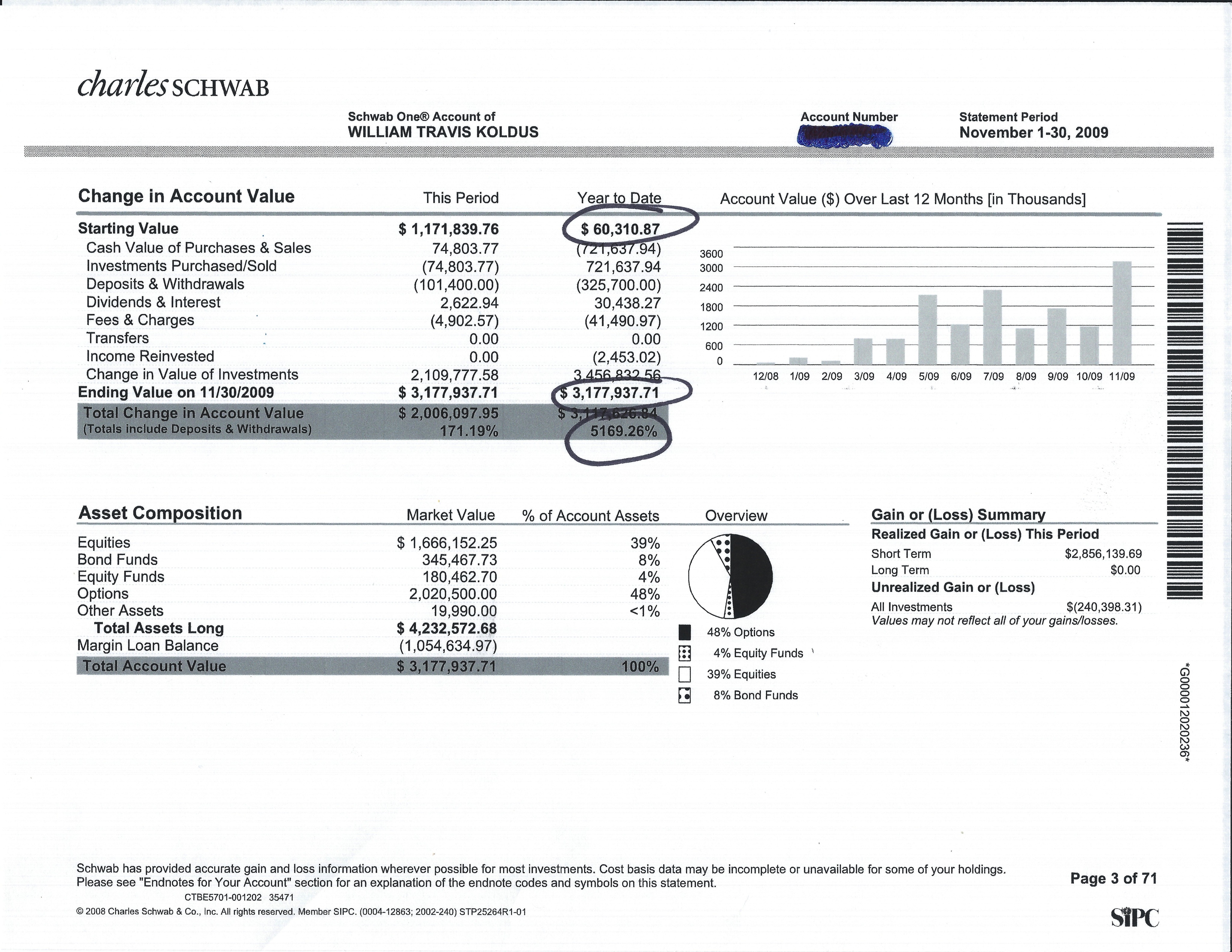

Security signifies the difference between the current ount you borrowed from into the their mortgage, and it can getting a valuable asset to view dollars whenever you need it. Scraping equity are a particularly appealing selection for property owners exactly who are flush which have home security once home values leaped from inside the present decades. With respect to the Government Reserve Financial out-of St. Louis, this new average home speed has actually increased off $327,000 prior to the fresh pandemic so you can a median price of $436,800 in the first one-fourth regarding 2023.

Although not, experiencing your residence guarantee isn’t really always a good idea, like whenever rates of interest is large or once you bundle to utilize continues to pay for a secondary or any other optional expenses. Remember, household equity financing and you will family security credit lines (HELOCs) was secure by your household, meaning you can treat your home if you can’t build the monthly home loan repayments. As a result, it’s imperative to just do it very carefully in relation to making use of your family equity. Listed here are six grounds to not ever availability your residence guarantee Clayton loans.

step one. Interest levels Try High

![]()

Already, our company is experience a period of highest interest levels because the Federal Reserve has grown prices ten times because as a way to curb rising cost of living. If Fed nature hikes interest rates, rates of interest towards the domestic equity factors in addition to often rise.

Despite times of low interest rates, interest rates to your domestic equity loans, HELOCs and cash-out refinances are usually more than number one mortgage loans. And more than HELOCs-and you can certain kinds of mortgages-have variable interest levels, so that you will never be protected against upcoming hikes in the event your obtain all of them whenever rates of interest was lowest. In the event that pricing go up rather from when your refinance or availability your domestic collateral, and also make your instalments could become more complicated.

Pricing on the funds and you can personal lines of credit would be even higher in the event your credit history is actually lower than better. Hence, it might make sense to hold off with the property collateral borrowing unit until it’s possible to replace your borrowing and/or Given begins to down prices (or both).

dos. We need to Continue Vacation otherwise Spend a huge Recommended Costs

As a general rule, a knowledgeable-situation circumstance to take to the debt is when it will help you grow your money if not improve your financial position. Such as for example, a mortgage makes it possible to purchase a property that can enjoy inside the worthy of through the years, and an educatonal loan makes it possible to rating an education you to advances your own long-label getting possible.

Therefore, borrowing from the bank money to possess a critical debts wonderful travel or wedding might not be an informed strategy. While you are this type of costs can be extremely important, they don’t alter your economic wellness. Think ahead of credit currency to cover elective expenditures. These experience are brief-existed, however the obligations your bear lasts for decades otherwise decades. The cash spent towards the mortgage costs could be better invested in other places, such as to suit your senior years otherwise building an emergency loans.

step 3. You want Have fun with Family Collateral to expend College tuition

Your have likely better options to pay money for higher education than leveraging your own home’s collateral. Try to exhaust most of the readily available scholarships, features and you can federal student assistance prior to turning to more pricey loan choice such as for instance personal student education loans or family security money. You don’t have to pay federal provides and you may grants, and government student loans fundamentally come with straight down rates than just family security investment, versatile payment arrangements and you may potential education loan forgiveness.

Home guarantee loans and you can HELOCs over the years have straight down interest rates than private college loans. not, their rates were closure the pit, and advantageous asset of straight down interest rates may possibly not be because the tall since prior to.